Skip hours of research. Our experts have tested dozens of trading bots so you don’t have to. Answer 6 quick questions and get a personalized recommendation based on your trading style and goals.”

What Is Slippage in Trading and How Do Bots Handle It?

Every trader eventually learns about slippage the hard way. You place an order expecting to buy at a certain price, and by the time the order executes, the price has moved. The difference between what you expected to pay and what you actually paid is slippage. It sounds minor, and in any individual trade it often is. But across hundreds or thousands of trades, slippage adds up into a meaningful drag on returns that can turn a profitable strategy into a losing one. What is a trading bot? It is software that automates the execution of trading strategies. How well a trading bot handles slippage is one of the most important practical factors that separates a bot that performs in live markets from one that only looks good in backtests. For more on how automated trading works, visit TradingBotExperts.com.

This guide explains what slippage is, why it happens, how it affects automated trading strategies, and what well-designed trading bots do to manage it.

What Is Slippage?

Slippage is the difference between the price at which you intended to execute a trade and the price at which it actually executed. If you place a market order to buy a stock at $50.00 and the order fills at $50.08, you have experienced eight cents of slippage per share. If you are buying a thousand shares, that is $80 of unplanned cost on a single trade.

Slippage can be positive or negative. Negative slippage, sometimes called adverse slippage, means you paid more than expected when buying or received less than expected when selling. Positive slippage means the trade executed at a better price than the one you targeted. Positive slippage is less common but does occur, particularly in fast-moving markets where prices move favorably between the moment you place your order and the moment it executes.

Slippage is a normal feature of financial markets, not an error or malfunction. It is a consequence of the way order matching works and the fundamental reality that prices are constantly changing. Understanding where slippage comes from helps traders design strategies and bots that account for it realistically.

Why Does Slippage Happen?

The most common cause of slippage is the gap between the price quoted when an order is placed and the price available when the order reaches the exchange and gets matched. This gap exists because prices change continuously, and there is always some time between when a trader decides to act and when the exchange processes the order. The faster the market is moving and the longer the delay in execution, the larger this gap can be.

A second major cause is liquidity. Every market has a certain depth of available orders at each price level. If you place a large buy order and there are not enough sellers at the price you want, your order will walk up the order book, filling at progressively higher prices until the full order is complete. This is known as market impact, and it is a form of slippage that becomes more significant as order size increases relative to the available liquidity at that price level.

Volatility also amplifies slippage. In a fast-moving market, prices can change by significant amounts in the fraction of a second it takes for an order to be placed and processed. Earnings announcements, major economic data releases, and sudden news events are common triggers for the kind of rapid price movement that produces large slippage on orders placed at market price.

According to research published by Investopedia, slippage is particularly prevalent in fast-moving markets and is a key consideration for any trader using market orders. For algorithmic traders, it is one of the primary reasons why backtest performance often overstates what a strategy actually delivers in live trading.

Slippage has a particularly significant impact on automated trading because bots typically execute a high volume of trades, and the cumulative effect of small amounts of slippage per trade can dramatically erode the profitability of a strategy over time.

This is where the gap between backtesting and live trading becomes most visible. Most basic backtesting frameworks assume perfect execution: every order fills at exactly the price the signal triggered. In reality, market orders almost never fill at exactly that price. When you add up the slippage across every trade a bot executes over weeks or months, the total cost can easily exceed what the backtest projected as profit, particularly for strategies that rely on small per-trade gains at high frequency.

Scalping strategies, which aim to capture small price movements many times per day, are especially sensitive to slippage. A strategy that targets two or three ticks of profit per trade cannot survive if slippage consistently eats one or two of those ticks. High-frequency approaches that look compelling on paper often fail in live markets primarily because their designers did not model slippage realistically.

Longer-term strategies with larger profit targets per trade are generally less sensitive to slippage, because the slippage cost represents a smaller proportion of the total expected gain. A strategy targeting a two percent move in a position can absorb a few basis points of slippage without material damage to its overall edge.

How Trading Bots Are Designed to Handle Slippage

Get the Top 5 Bots for Early Retirement report:

Well-designed trading bots use several techniques to manage and minimise slippage. Understanding these techniques helps traders evaluate the bots they use and set realistic expectations for live performance.

Limit orders instead of market orders. The most fundamental slippage control is the choice of order type. A market order instructs the exchange to execute the trade immediately at the best available price, which can be different from the current quoted price, particularly in fast or illiquid markets. A limit order specifies a maximum price for a buy or a minimum price for a sell, guaranteeing that the order will not execute at a worse price than specified. The trade-off is that limit orders may not fill at all if the market moves away before the order can be matched. Well-designed bots balance the need for execution certainty against the cost of slippage, using limit orders where the strategy permits and market orders only where immediate execution is essential.

Order splitting. Rather than placing a single large order that will walk up the order book and generate significant market impact, sophisticated bots can split large orders into smaller pieces that are executed over time. This approach reduces the market impact component of slippage by giving the order book time to replenish between fills. The cost is that the average fill price may change during the execution period if the market moves directionally, which introduces a different kind of execution risk.

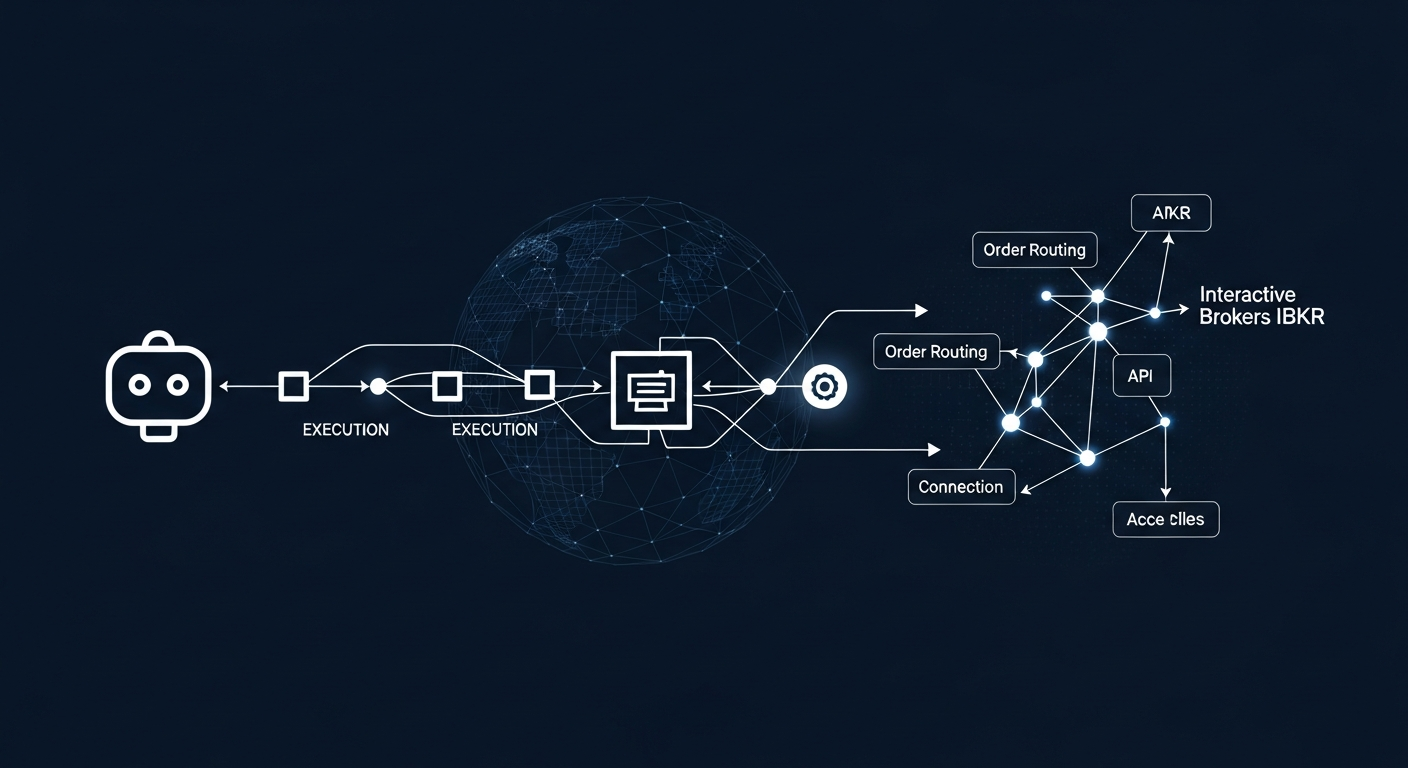

Execution algorithms. More advanced bots use execution algorithms like VWAP (Volume Weighted Average Price) or TWAP (Time Weighted Average Price) to spread order execution across time in a way that minimises deviation from benchmark prices. These algorithms are standard in institutional trading and are increasingly available to sophisticated retail traders through API-connected brokers.

Liquidity filtering. Some bots include logic that checks order book depth before placing a trade, and either delays or reduces the size of a trade if there is insufficient liquidity at the target price to fill the order without significant slippage. This approach prevents the bot from entering trades in conditions where execution quality is likely to be poor.

Slippage modelling in backtests. Responsible strategy development includes realistic slippage assumptions built into the backtesting framework. Rather than assuming perfect fills, the backtest adds a fixed or variable slippage estimate to every trade. This produces a more conservative and realistic picture of expected performance, and reduces the disappointment of seeing live results fall short of backtest projections.

The amount of slippage a trader is likely to experience varies significantly depending on the market they are trading. Understanding these differences helps in choosing the right market for a given strategy and calibrating slippage expectations appropriately.

Major equity markets and large-cap stocks tend to have deep order books and tight bid-ask spreads, which means slippage on retail-sized orders is usually modest. Trading the most liquid instruments in the most liquid hours of the trading day is one of the simplest ways to minimise slippage.

Cryptocurrency markets present a more variable picture. Major pairs like Bitcoin and Ethereum on the largest exchanges have reasonable liquidity during active trading hours, but liquidity can dry up quickly in smaller tokens or during off-peak hours. The volatility that attracts many traders to crypto also means that prices can move significantly during the time it takes for an order to be processed, producing larger slippage than traders accustomed to equity markets might expect.

Options markets have their own slippage dynamics. Because options contracts typically have wider bid-ask spreads than the underlying stock or ETF, the cost of entering and exiting options positions via market orders can be substantial. Options traders using automated systems almost always rely on limit orders with specific price targets rather than market orders, accepting the risk of non-execution in exchange for protection against wide spreads.

Take Our Free Trading Bot Match Quiz

Whether you are just starting to explore automated trading or evaluating bots for a more serious systematic approach, understanding how a bot handles execution quality and slippage is one of the most important questions to ask.

Find Your Best Trading Bot in 60 Seconds

Which trading bot is right for you? Take our free Trading Bot Match Quiz and get a personalised recommendation based on your budget, goals, and risk tolerance in under 60 seconds. We will also send you a free e-book with honest reviews, performance stats, and red flags to avoid in the trading bot world. Whether you are trading stocks, options, or crypto, this guide helps you find the right platform to get started. Click here to take the quiz and get your free report.

Questions to Ask Yourself Right Now

Does the bot or strategy you are using account for realistic slippage in its backtests, or does it assume perfect fills?

Are you trading in markets and at times of day where liquidity is sufficient to minimise slippage at your order size?

Does the bot use limit orders where appropriate, or does it rely on market orders that expose every trade to adverse slippage?

Have you compared your live fill prices to the prices your strategy targeted to understand your actual slippage costs?

Free Report

Before You Choose a Bot, Read This

Get our free Top 5 Bots for Early Retirement report plus The Bot Report newsletter — the bots we'd actually trust to compound over the long term.

Written by

Priya Nair

9 min read

The TradingBotExperts Editorial Team consists of traders, analysts, financial writers, and AI researchers with over a decade of combined experience in algorithmic trading and fintech. We produce research-driven content to help traders understand automated systems, evaluate trading bots, and navigate the evolving world of AI-powered investing.

How to Choose the Best Trading Bots for Your Strategy

Take our free quiz to show how to pick bots that actually work for you

Get My Free Bot Report

Get Our Expert Bot Recommendation

Skip hours of research. Our experts have tested dozens of trading bots so you don’t have to. Answer 6 quick questions and get a personalized recommendation based on your trading style and goals.”

Join The Bot Report newsletter and get our free guide to the five trading bots most likely to help you retire early — backed by real reviews and verified performance.